Hello from Nicole and the team at ngoLAW, and, coming in just under deadline, this is our 2026 first quarter ngoLAW Brief.

In this ngoLAW Brief we deal with some topical and technical issues:

- Report from the coalface- the new online SARS exemption application process

- Hot off the press: Update on the General Laws Amendment Bill and its impact on non-profits

- Some thoughts on ‘independent directors’ and what they are useful for

- The SARS Penalties- what the actual?

- The SARS Fiduciary Trio- myth busted

First, some pics from our year-end lunch at the fabulous Surf Riders Cabanas Umhlanga:

SARS NEW ONLINE PROCESS: PROGRESS AND LIMITS

As mentioned in our September 2025 ngoLAWBrief, https://ngolawsa.co.za/ngolaw-brief-september-2025/ the new SARS online PBO application service went live for the public on 1 March 2026.

This new service means that, while new applications lodged via email or courier prior to 1 February 2026 (when ‘manual’ services were closed) will still be processed ‘manually’, from 1 March 2026 the only way to apply for any type of income tax exemption is via the SARS efiling platform.

The major impacts of the transition are, in our experience so far:

- Speed

Then: the promised turnaround time under the old system as 52 working days (2 months) but actual turnaround was closer to 6 months.

Now: The promised turnaround is 21 working days, but actual turnaround (from lodging to granting or to receipt of a query) is anywhere between 24 hours and 1 week! We suspect that the current lightning-fast times are partly due to the newness of the system, and that those who only make these applications intermittently will still be figuring out how to navigate the new system.

We were fortunate to be part of the SARS testing phase, so were guided through some test applications made.

- Fewer documents to upload

- The EI1 is no longer required, as it is now an online form;

- SARS Registered Representative documents do not have to be lodged, as the Registered Representative must be appointed (and the efiling profile set up) before an application can be made;

- For NPCs, there is a link to the CIPC system, so no CIPC documents verifying directors need be uploaded.

- Bank account required

- Under the manual system, the application could be processed prior to the opening of a bank account. Under the online system, banking details are mandatory, and the application cannot proceed without them.

- More information needed: some examples

- The old application form had space for just three governing body members details- the new process requires that all of the board’s details are recorded

- You need to figure out and include the ‘sector code’ for the work of the organisation (not too easy to figure out!)

- You include a declaration that no board members have been disqualified from service on a board;

- It requires information on whether the organisation conducts certain activities outside of SA (to figure out whether NPO status is compulsory)

From the coalface, we can report that there have been hiccups and technical issues and some of these are yet to be ironed out. But, in comparison with systems rolled out by other departments (DSD!) and considering the complexity of the exemption laws and the variables to be taken into account, SARS has really put their back into the testing and refining, and taking comments and input.

New applications for NPCs are working really well, with the odd hitch when drawing details from CIPC. We are finding that applications to update documents and details (such as an amended founding document, or a request to add another status) are not as seamless, and some of these seem to be getting stuck.

The new system does not yet allow appeals and objections to be captured (these must still be lodged via email).

We will keep you posted on progress and any new information on this score.

FATF IS BACK: ANOTHER ROUND WITH A GLAB

Dancing to the FATF tune is, it turns out, not a one-time gig, but something that needs to be choreographed and orchestrated every couple of years, as review processes just keep rolling around. Although SA was released from Grey-Listing on 24 October 2025, the new review cycle for SA begins again in mid-2026, with an on-site FATF inspection and audit in April 2027.

In preparation for this next round of reviews, and with the aim of staying off that dreaded Grey List, a General Laws (Anti-Money Laundering and Combating Terrorism Financing) Amendment Bill, 2025 was issued by National Treasury on 15 January 2026, with the deadline for comments initially being 13 February 2026.

In the first version of the Bill the proposed amendments to the NPO Act were few in number, but clumsily done, and, in a bid to satisfy FATF, specifically added reference to the powers to “monitor and enforce compliance” being given to the NPO Directorate. As the NPO Act is primarily framed as creating an enabling and supportive framework for nonprofits, this sort of wording was alarming. And especially as they were applicable not just to the categories of organisation for whom NPO registration became compulsory under the 2022 GLAB, but to all nonprofits in South Africa.

After submissions from civil society and Allison Tilley’s GroundUp piece https://groundup.org.za/article/alarming-new-bill-seeks-to-police-non-profit-organisations/#:~:text=Section%205%20of%20the%20act,assisting%20compliance%20to%20policing%20it, the deadline for submissions was extended to 2 March, and the NPO Working Group and other civil society friends had various engagements with DSD, Treasury and the drafters of the Bill.

Rewind: for those not paying attention at the time, the “Octopus Bill” of 2022 attempted, amongst other things, to make NPO registration compulsory for every single organisation operating in South Africa. This broad-brush approach was not actually required by FATF, would not have achieved the oversight of ‘risky’ organisations which was sought, and would have broken an already faltering DSD. Importantly, it was also unconstitutional. Our submissions on these matters were heard, and the requirement for compulsory NPO status was confined to organisations doing certain sorts of work which also operate or provide funds outside of South Africa. For some of the history read: https://ngolawsa.co.za/last-quarter-2022-ngolaw-in-brief/

Elsewhere in the world and on our continent, governments went ‘how high?’ when jumping through the FATF hoops and took the opportunity to pass laws which gave these governments control over who could set up nonprofits and what work they could. LGBTQI+ organisations were particularly targeted by some, as well as organisations calling out corruption or political abuse. For those interested in learning about or joining the fight against these ‘unintended’ consequences of FATF, go to the Global NPO Coalition on FATF https://fatfplatform.org/

We are happy to report that, after our engagements with the drafters at DSD and Treasury, some of our message has landed, and the latest iteration of the Bill, which has been fast tracked was put before Parliament on 27 May 2026. This version corrects the drafting errors in the previous version, so that it is clear that that it is only the class of organisations who are legally required to register who are subject to non-compliance oversight and administrative penalties.

To read the entire Bill go to General Laws (Anti-Money Laundering and Combating Terrorism Financing) Amendment Bill | PMG

The Bill will now go to Parliamentary Committees. It is in this Committee stage that there will again be opportunity for final comments and submissions.

Watch this space for updates.

“INDEPENDENT” DIRECTORS: WHAT ARE THEY? AND DO WE NEED THEM?

The first governing boards of nonprofits are often made up of people who are founders or passionate supporters of the founders. And there is nothing wrong with this, as it takes concerted effort and a huge time investment to get a new nonprofit successfully launched. The Founder Board are generally rolling up their sleeves and playing the part of both board and executives/ management, until funding comes in to employ people to manage and execute on the vision.

One component of the evolution from Founder Board is the letting go of executive powers, stepping back from administration, and settling into the oversight and governing role that a board is meant to play. Along with this should come an awareness of the need to engage in succession planning (making sure that the baton is incrementally and sensibly passed to the next board) and consideration of the ideal board composition and whether the board could do with some ‘independent’ directors.

The inclusion of ‘independent’ directors on the board is widely regarded as a safety mechanism against possibly collusive (or just too comfortable) ‘insiders’, and as bringing valuable outside or fresh perspective to the work of the board. It has become a component of credibility for many, especially as it is included in all governance guides and codes as an essential element of good governance.

The widely influential King Codes (King V effective from 1 January 2026) has this to say about the ideal composition of governing bodies:

“The governing body ensures that its composition is balanced with respect to the mix of competencies, diversity and independence that enables it to discharge its obligations objectively and effectively.”

Regarding the classification as ‘independent’ King V advises that:

“The governing body may categorise its non-executive members as independent if it concludes that there, is no interest, position, association or relationship which, when judged from the perspective of a reasonable and informed third party, is likely to unduly influence or cause bias in decision making in the best interests of the organisation”

This King V definition of an ‘independent’ director is referred to in the B-BBEE Codes, specifically in the part which deals with the “Flow-through” of B-BBEE status. Simply put, an NGO can have level one B-BBEE status based on the racial composition of its beneficiaries alone. However, if the NGO owns shares in a commercial company, that prime B-BBEE status can only ‘flow through’ to the subsidiary if, amongst other factors, 50% of the board are ‘independent’. So in the case of a B-BBEE flow-through model, independent directors are mandatory.

For all other organisations they are a factor in assessing credibility of an organisation. And the King V Guidance Note to its application to nonprofits recognises this https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/CFA6E544-15F6-4FE2-900F-872F39A21B52/Non-Profit_Organisation_Application_of_King_V.pdf

“The governing body should be composed of individuals with the necessary mix of competencies, diversity and personal qualities to enable it to discharge its responsibilities effectively. A balance between professional expertise and stakeholder insight is often required.

Where governing body members are appointed as representatives of specific stakeholders—such as donors, beneficiaries or affiliated institutions—care should be taken to preserve independence and objectivity in decision making and collective accountability.

NPOs may face challenges attracting independent professionals due to resource limitations or their inability to offer competitive remuneration. However, they are encouraged to approach professional associations, academic institutions or volunteer networks to source suitable individuals willing to serve, in many instances, pro bono or at minimal compensation. Independence of mind and freedom from conflicts remain critical, regardless of whether members are appointed internally or externally.”

However, it is important to note that it is not just those who pass the test of being ‘independent’ directors who have to act with independence. The essence of the fiduciary duty is that you have a custodial duty, acting not in your own interest, but in the interest of the organisation that you serve.

So, no matter what gets you into the room, once you are on a board you are required to remove your other hats, and do your duty toward this organisation you serve.

As King V says, the individual members of the board have the responsibility:

“to exercise independence of mind and have the courage to speak up when necessary”

THE SARS PENALTIES: WHAT?

We are receiving messages from many client about their being deluged with SARS notices on penalties being levied, and rapidly escalating interest, even for long-dormant organisations.

SARS is invoking section 210 of the Tax Admin Act which allows it to impose monthly penalties for non-compliance, for as long as the non-compliance continues.

To our mind, the reasons that this is occurring now are:

- SARS has been on a major push to increase their tax recoveries. These penalties, the interest which builds up on them and then the actual tax which may be paid because of the need to stop the penalties building up, is a big part of that plan;

- The increased granularity, interoperability and efficiency of the SARS systems have created ability and capacity to impose these penalties and chase down the non-compliers.

The minimum penalty amount is R250 per month, even if there is no tax owed, but returns have just not been filed.

SARS embarked on a rollout to chase down non-compliant trusts from 4 May 2026, and the following is from their website announcement:

2 April 2026 – On 27 March 2026, a public notice was issued listing the non-submission of income tax returns by Trusts as an incidence of non-compliance subject to an administrative non-compliance penalty under section 211 of the Tax Administration Act, 2011 (TAA). Administrative penalties may be imposed on taxpayers who fail to comply with an obligation under a tax Act. The penalties are designed to encourage compliance, applied consistently, and may recur monthly until corrected.

From 4 May 2026 SARS will issue a penalty assessment notice (AP34) to notify taxpayers of administrative non-compliance penalties that have been imposed for non-compliance with regard to outstanding trust income tax returns. The penalty assessment notice will reflect imposed penalties, outstanding income tax returns for which tax periods, and corrective measure to be followed to prevent recurring penalties. Taxpayers are also advised to submit a request for remission if they do not agree with the penalty imposition. This penalty will apply to trusts with outstanding income tax returns (ITR12T) for tax periods from 2024 onwards. For more information, see the updated Guide to submit a dispute via eFiling.

Kindly note that the previous Guide called ‘How to dispute Administrative Penalties via eFiling’ has been incorporated into the above guide.

Also see our step-by step video on How to file a Request for Remission for Trust on eFiling.

Following an outcry from dormant trusts who received notices and penalties, SARS published the following (with my emphasis):

9 April 2026 – The South African Revenue Service (SARS) is reminding all trusts registered in South Africa that, in terms of tax legislation, they are required to submit Income Tax Returns for every year of assessment. This obligation applies even where a trust had no economic activity during the relevant year.

Where a trust is no longer being used for its intended purpose, trustees are encouraged to formally terminate the trust through the Office of the Master of the High Court (Master). Once the Master has issued a written confirmation of termination, trustees should request SARS to deregister the trust for income tax purposes. This process assists in preventing the unnecessary imposition of administrative penalties arising from ongoing non-compliance.

Although the Trust Property Control Act does not expressly prescribe a deregistration process, the Chief Master issued a directive in 2017 to provide clarity on the procedure to be followed. Importantly, trustees must first establish and regularise the trust’s tax compliance status with SARS before approaching the Master for termination.

Trustees act as representative taxpayers of a trust in terms of the Income Tax Act and are required to ensure that all outstanding tax returns, payments, and related tax obligations are fully resolved prior to requesting termination at the Master and deregistration at SARS. In some instances, SARS may owe a trust a tax refund. Once a trust has been terminated by the Master, it legally ceases to exist, as does the Office of Trusteeship. In such circumstances, SARS is unable to lawfully process or pay any refunds due to the trust.

Trustees are therefore urged to follow the correct sequence

- first confirm and regularise the trust’s tax affairs with SARS, and

- only thereafter proceed with termination at the Master.

This approach safeguards compliance and protects trustees from potential personal liability. This also ensures that any refunds due to the trust can be processed timeously.

THE MYTH BUSTED: THE TRIO OF SARS FIDUCIARIES

SARS tax exemption application and the three ‘fiduciaries’:

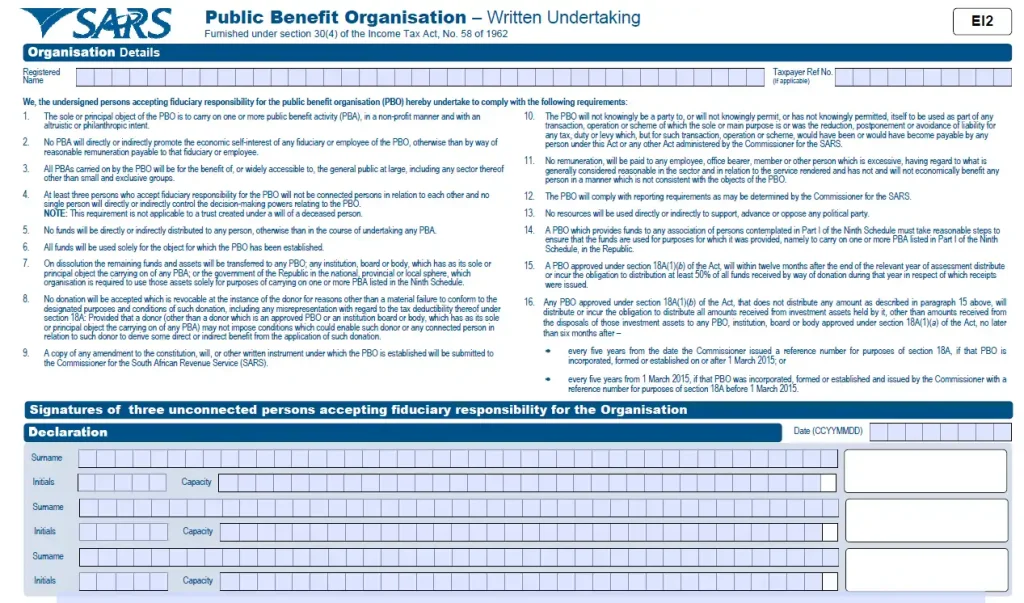

Historically, the SARS documents which were required to be submitted with tax exemption applications, referred to those who signed them as ‘fiduciaries’. And, as those forms only had space for the details of three people and their signatures, only three of these ‘fiduciaries’ provided their details, and gave an undertaking (on a form called the EI2) that, if the founding document of the organisation did not contain the clauses required by section 30 of the Income Tax Act, they would ensure that it abided by those provisions.

In the Income Tax Act, 1962, the section which deals in detail with public benefit organisation (PBO) status, has this requirement in s30(2)(b)(i)

[A PBO is] required to have at least three natural persons, who are not connected persons in relation to each other, to accept the fiduciary responsibility of such organisation;

The Income Tax Act does not define ‘persons [who have] fiduciary responsibility’ but it does not need to, as the idea of a ‘fiduciary’ is well established and understood in our law.

What/who is a fiduciary?

A “fiduciary” is simply someone who holds a position of trust, someone who takes care of the property or interests of another. The word ‘fiduciary’ comes from the Latin ‘fiducia’, which means ‘confidence, trust, assurance’.

Those who are in a custodial position of trust are under a ‘fiduciary duty’.

All trustees of trusts, directors of companies and governing boards of voluntary associations are under this duty. The nature of the duty of those who hold these roles is established under common law, and has been incorporated into statutes such as the Companies Act 71 of 2008 and the Trust Property Control Act of 1988.

(What many do not realise is that it is not only those who are official members of boards who are under a ‘fiduciary duty’. Employees are under a fiduciary duty to their employees, agents to those they act on behalf of, lawyers to those they represent: anyone who is taking care of the assets or interests of another is under the fiduciary duty.)

The essence of the fiduciary duty is that one is legally bound to act in good faith, with loyalty, and in the best interests of another party, avoiding conflicts of interest and personal gain at the expense of those they serve. A fiduciary is required to apply the degree of care and skill in the execution of their duties as may reasonably be expected of a person taking care of the property or affairs of another.

The fiduciaries undertaking to SARS

From the year 2000 (when the new PBO tax exemption became law) until an amendment in 2014, Section 30(4) of the Income Tax Act provided that, if the founding document of an organisation making an application for tax exemption did not contain the clauses made mandatory by section 30(3)(b), the organisation was ‘deemed’ to comply if it submitted an undertaking to comply. This undertaking was form EI2, and was signed by the same three ‘fiduciaries’ who signed the main application form.

After 2014, when the law changed to make the ‘deemed to comply’ provision only applicable to those who could not amend their founding documents (will trusts and branches of foreign organisations) the EI2 form continued to be routinely submitted and accepted by SARS for all applications, and the SARS exemption letters regularly gave a date after approval date by which exempt organisations of all types needed to amend their founding documents if they did not contain the relevant clauses. (This continuation of acceptance of the EI2 was practically very useful to those making applications. During a time when SARS typically took 4 to 6 months to process applications, avoiding the additional delay of first amending the founding document was often important to applicants for the status.)

It is from this EI2 undertaking and fact that the forms give room for only three of those on the board/committee/governing body to sign, that the myth of the “3 SARS fiduciaries” arose. Because of the forms, there are many who believe that only those three whose names and signatures were on the EI1 and EI2 forms, were responsible to SARS for the organisation’s adherence to the provisions of the relevant sections of the Income Tax Act.

Who is responsible to SARS?

Even during the period 2000-2014, when the EI2 form required three people to sign it to declare that the organisation would comply, these three were never doing so alone and were never under a greater duty or burden than those left off the form.

Although section 30(4) refers to section 30(3)(b)(i) which requires that the board/ committee/ governing body should be made up of at least three’ unconnected (not related to each other) people who ‘accept fiduciary responsibility of such organisation’, in my view it is not saying that only three of those who are on the board/committee/governing body ‘accept the fiduciary responsibility. It is clear in our law that all of the people appointed a board of an organisation are under a fiduciary duty and so are ‘fiduciaries’.

The past signing of the SARS EI2 form did not increase or amplify the standard fiduciary duty but merely listed and identified three of the ‘fiduciaries’.

The three who signed the document gave an undertaking that the organisation would be administered in compliance with the SARS rules set out in the EI2 document. In my view this undertaking was given by these three not as individuals, but as board members, and so on behalf of the organisation as a whole.

It is important to note that it is now, and has always been, a requirement of PBO status that the SARS rules are incorporated in the founding/governing document (constitution/ trust deed/ memorandum of incorporation (MOI)) of the organisation. All of those who are directors/trustees/committee members are bound by the provisions of the founding document and must exercise their powers strictly in accordance with its provisions.

Therefore all who serve an organisation, whether they are on the board or are employees or other officers of the organisation already have to abide by the constitution/ trust deed/MOI, so the burden of compliance with the SARS provisions is not, and has never been, only on the trio who may have signed the EI2 form, but on all who are under a fiduciary duty to the organisation and its ultimate beneficiaries.

Keep the questions coming and send us suggestions for future topics – visit our website, hit the ‘contact’ tab, and enter your question into the ‘Contact Form’ space provided.

Aluta continua

Nicole, Bandile, Janice, Chelsea, Lisa, Alison, Asanda, Ayanda and Dorothy

{kind=link}

{kind=link}